Side letter agreements are a common way to agree on special conditions granted to certain investors concerning private investment funds. Fund managers should be familiar with the practices and the regulation relating to side letters and exercise caution when approving side letter requests.

30.12.2022

Side letter agreements require expertise and diligence from the fund manager

What is a side letter?

Side letters are used particularly in conjunction with closed-end funds where the negotiation of the contract provisions is of high importance, considering that the rights to withdraw from such funds are limited and that the structure of these funds is complex. Open-ended funds (such as hedge funds) also typically utilise side letters, for example when a seed investor or cornerstone investor who is subject to special tax or regulation requirements is making a significant investment and requires customised special conditions.

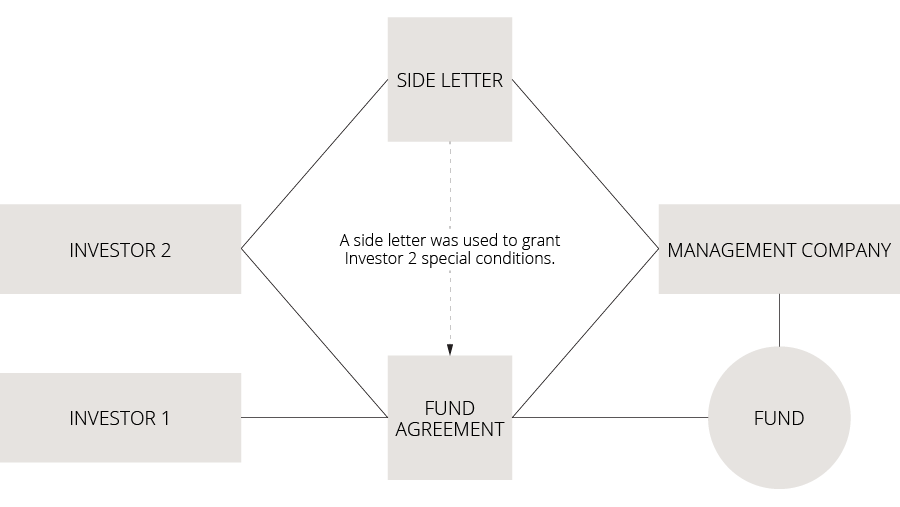

A side letter can be used to supplement and amend the provisions of a fund’s constitutional document (such as the fund agreement of a limited partnership fund). Side letters are typically required when an investor has particular commercial, legal, tax-related or operative concerns about investing in a fund. Sometimes a side letter is mandatory so that the investor can join the fund in the first place due to the special provisions applied to the investor or the commitments the investor has made to other parties (such as the investor’s own investors). On the other hand, the investor often has an incentive to negotiate a set of agreements that suits them best both commercially and legally.

The parties to a side letter

If the fund is structured as a limited partnership, side letter arrangements are typically made between a general partner acting on behalf of the fund and individual investors. If the fund is a Finnish special investment fund, the parties to the side letter are the investor and the alternative investment fund manager on behalf of the special investment fund. In limited partnership funds, some investors can request that the alternative investment fund manager and the investment manager become additional parties to the side letter in order to facilitate the enforcement of the provisions concerning the operations of the said parties. Therefore, side letters should be drafted carefully to ensure that the correct parties are bound by them.

A fund agreement may not be amended without the consent of the investors unless it is specifically provided for in the fund agreement. This being the case, while a side letter can be used to amend certain provisions of the fund agreement between a general partner and an individual investor, it cannot be used to supersede the interests of other investors or to amend the fund agreement in relation to other investors.

The right to make side letters must be provided for in the fund agreement

The fund agreement must include a provision that explicitly allows the fund’s general partner and individual investors to enter into side letter agreements that change the conditions of the said investor’s fund investment in relation to the provisions under the fund agreement. The explicit authorisations for entering into side letter agreements that are provided for in the fund agreement play an important role, particularly when foreign institutional investors demand separate legal opinions on the enforceability of side letters.

The fund agreement clause authorising the making of side letters can limit the special conditions that a general partner may grant the investors, although the market practice is to draft the authorisation clause to be very broad. In any case, this clause must allow not only side letters but also the types of conditions that the general partner can propose to the investors (or at least it should not prohibit them).

Regulation ensures the equal treatment of investors

In addition to the commercial and practical aspects of making side letters, fund managers should pay attention to the associated regulatory issues. Fund managers must comply with provisions on preferential treatment of the Alternative Investment Fund Managers Directive (2011/61/EU, ‘AIFMD’) which have been implemented into to the Act on Alternative Investment Fund Managers (7 March 2014/162). Pursuant to the AIFMD, investors must be provided with ‘a description of how the AIFM ensures a fair treatment of investors and, whenever an investor obtains preferential treatment or the right to obtain preferential treatment, a description of that preferential treatment, the type of investors who obtain such preferential treatment and, where relevant, their legal or economic links with the AIF or AIFM’. This disclosure obligation is in force before the investment is made and also after any material changes to the preferential treatment. There are several ways to carry out the disclosure obligation.

Legal risks associated with side letters

The most important goals of fund managers are to raise capital and to acquire new investors. They might therefore be very tempted to approve side letter requests from investors who are ready to make a large investment in the fund. This kind of situation may be at hand particularly when an investor demands a side letter just before the fund is closed, allowing the investor to gain an advantage on the fund manager due to urgency. The risks associated with side letters should be kept in mind when negotiating and drafting them.

First, it is important to understand that once a side letter is made, the fund manager may have two competing obligations: 1) the obligations towards all investors pursuant to the fund agreement, and 2) the obligations towards an individual investor pursuant to the side letter. In a conflict situation, the provisions of the side letter will generally prevail. The fund manager can usually balance these competing obligations. For example, if the fund manager waives their fee with respect to a specific investor in full or in part, usually there will be no significant conflict as the exception does not have a detrimental impact on the other investors.

However, some common side letter arrangements may cause potential legal problems to fund managers. If, for example, the side letter allows an investor to withdraw from the fund prematurely, the fund manager may need to respond to an action on not fulfilling their duty of care towards the other investors as the other investors can claim that the side letter has put them in a materially unfavourable position. Legal evaluation is also necessary for such side letter conditions that grant the investor rights to the distribution of funds deviating from the fund agreement or that mitigate the investor’s payment obligations towards the fund, as this might lead to an increase the other investors’ relative payment obligations.

Prepare for side letter arrangements in advance and draft them carefully in writing

Although fund managers may be tempted to approve side letter requests, it is recommended to use appropriate consideration and care in approving the requests. A clear strategy for side letters should be a part of the fund establishment from the start. It is recommended to prepare a roadmap that determines the most likely recipients of side letters and the conditions they may be granted.

The fund’s constitutional document, and preferably the private placement memorandum as well, should contain an appropriately formulated clause to inform the investors that the fund manager can make side letters with individual investors.

Fund managers must also ensure that they do not make oral agreements. All side letters that concern amending or supplementing the fund agreement provisions should be made in writing. Often the investors asking for side letters will require this in any case, but it is important for fund managers to refrain from making vague promises. This also applies to any email correspondence between the fund manager and a potential investor on the interpretation of the fund agreement provisions. It can be unclear whether this constitutes a binding agreement.

When assessing each side letter request, the main concern of fund managers is to see whether the conditions of the proposed side letter impact their duty of care towards the other investors. If the conditions of the side letter do not affect the other investors, there should be no trouble. The assessment of situations that are not as clear, such as the customised requirements of large foreign institutional investors, may require specialised legal advice.

Read our previous blogs on funds:

Special investment funds also work as closed-end funds – pay attention to special provisions

Latest insights

Article published 17.7.2026 – Real Estate Investments & Transactions

Special features of real estate transactions in Finland: Formal requirements, permit requirements and pre-emption rights

Article published 13.5.2026 – Venture Capital & Minority Investments

Newly launched Series Seed 4.0 is a comprehensive standard seed financing documentation for the Finnish market

Article published 13.5.2026 – Venture Capital & Minority Investments

Newly launched Series Seed 4.0 is a comprehensive standard seed financing documentation for the Finnish market

Article published 8.5.2026 – Environment, Energy & Green Transition

Reform of Finland’s land use legislation – key takeaways for project developers

Article published 8.5.2026 – Environment, Energy & Green Transition

Reform of Finland’s land use legislation – key takeaways for project developers

Article published 28.4.2026 – Private M&A

Unlocking value in carve-outs – Why integration planning deserves top priority in every carve-out

Article published 28.4.2026 – Private M&A

Unlocking value in carve-outs – Why integration planning deserves top priority in every carve-out

Jessica Salmia & Elina Marttala

Jarno Tanhuanpää, Tuomas Honkinen & Jussi Mäkikangas

Tarja Pirinen, Marius af Schultén & Joel Aartolahti

Benjamin Bade, Maiju Mäkinen & Samuli Salminen

Latest references

eQ Fund Management Company Ltd – Structural Arrangement Related to Residential Funds

We acted as legal advisor to eQ Fund Management Company Ltd in a structural arrangement in which Special Investment Fund eQ Residential Fund and Special Investment Fund eQ Residential Fund II transferred their assets to the newly launched Special Investment Fund eQ Residential Fund III. In connection with the arrangement, eQ Residential Fund III raised 37 million euros in new capital, and its fundraising will continue throughout 2025. The portfolio of eQ Residential Fund III consists of 19 residential properties completed between 2021 and 2024, comprising nearly 1,400 apartments located in the Helsinki Metropolitan Area, Turku, and Tampere.

Case published 21.5.2025

Finnish Climate Fund – Cornerstone investment in Taaleri Bioindustry I fund

We advised the Finnish Climate Fund as it invested in the alternative investment fund Taaleri Bioindustry I. The investment commitment of the Finnish Climate Fund was EUR 15 million. The Taaleri Bioindustry I fund supports the development of bioindustry primarily in Finland. The target fund is the first private equity fund in Europe that focuses purely on bioindustry projects. The fund is also one of Finland’s first private equity funds to be classified as dark green, i.e. funds under Article 9 of the EU’s Sustainable Finance Disclosure Regulation. We acted as a comprehensive advisor in drafting the documentation concerning the fund investment and in negotiations while taking into account the unique issues and requirements of the role of a cornerstone investor in the Finnish Climate Fund. When providing advice, we focused particularly on the SFDR and the dynamic and transient regulatory issues relating to compliance with the SFDR.

Case published 14.10.2022

Institutional Investors – Fund Investments

We advised and assisted our Finnish and international clients in dozens of fund investments in 2021. Our clients include pension institutions, asset management companies, fund management companies, foundations, private equity companies and listed companies. Individual fund investments amounted to approximately EUR 10–20 million on the average. Our advice related to both Finnish and foreign fund investments. The funds’ investment strategies varied mainly from different private equity funds (such as buyout, venture capital, private credit) to real property funds (such as real estate, infrastructure) and funds of funds, i.e. funds that invests in other types of funds using various strategies. Our task has been to ensure, in particular, that the commercial and administrative terms of the funds that are invested in are fair to the investor and are in line with customary market practice. To this end, we have negotiated the terms of the funds with fund managers. We have also ensured that the fund investment fulfils the constraints of national regulation applicable to our client and their potential investment policy. We have also advised our clients in other general issues that relate to the due diligence process of fund investments. We have also been actively assisting our clients in fund investments previously over the years. Our experts Antti Vepsä and Karlo Siirala discuss the specific issues relating to fund investments in their blog: Private Equity Fund Legal Due Diligence: How to Conduct It More Efficiently

Case published 31.1.2022

OP and Finnfund – Establishment of a New Global Impact Fund

We represented OP and Finnfund in the establishment of Finland’s first impact fund that will invest into emerging markets. The OP Finnfund Global Impact Fund I will promote the achievement of the UN Sustainable Development Goals in a measurable way while providing an attractive return for investors. As a new type of fund in the Finnish market, the fund will seek systematic and measurable impact, primarily by investing into projects in the fields of sustainable agriculture and forestry, renewable energy and financial institutions. The investments will support mitigating and adapting to climate change, creating sustainable employment, as well as safeguarding affordable and clean energy. The fund will invest in developing countries defined by the OECD. OP Fund Management Company Ltd will act as the Alternative Investment Fund Manager (AIFM) of the fund. OP Financial Group is Finland’s largest financial services group whose mission is to create sustainable prosperity, security and wellbeing for its owner-customers and in its operating region by means of its strong capital base and efficiency. OP Financial Group consists of 143 OP cooperative banks, its central cooperative OP Cooperative, and the latter’s subsidiaries and affiliates. The Group has a staff of 12,000 and 2 million owner-customers. Finnfund is a Finnish development financier and professional impact investor. Finnfund builds a sustainable world by investing in responsible and profitable businesses in developing countries. Each year Finnfund invests 200–250 million euros in 20–30 projects, emphasising renewable energy, sustainable forestry, sustainable agriculture and financial institutions. Today Finnfund’s investments and commitments total about 800 million euros, half of them in Africa. The company has approximately 80 employees.

Case published 5.5.2020